Let’s say you run a healthcare professional society. Your organization has many different revenue streams, including conferences, membership dues, educational workshops, sponsorships, and individual charitable donations.

After submitting your nonprofit’s Form 990 to confirm your tax-exempt status, you realize you forgot to report a significant donation from a major donor that wasn’t in your system. Not only have you risked noncompliance, but you also neglected to thank the donor for their contribution, potentially damaging your relationship with that supporter.

Amidst the chaos of running a professional society, proper accounting for nonprofits saves staff headaches, keeps your organization in good standing, and maintains strong stakeholder relationships. With 47% of nonprofits lacking the necessary funds to execute their programs and services, implementing strong financial management practices is more important than ever.

To help your nonprofit thrive, we’ll walk you through the basics of nonprofit accounting and cover expert tips:

- What is accounting for nonprofits?

- Core Nonprofit Financial Statements, Documents, and Reports

- 7 Nonprofit Accounting Expert Tips

- Specific Accounting Considerations for Associations

- Working with an Association Accounting Expert

What is accounting for nonprofits?

Accounting for nonprofits refers to how membership-based associations manage their finances through proper planning, recording, tracking, and reporting. While nonprofit accounting is similar to for-profit accounting in many ways, their differences stem from their varying goals.

For-profit accounting focuses on generating a profit and satisfying shareholders. On the other hand, nonprofit accounting is all about accountability. Since nonprofits rely on stakeholders like donors, members, grant funders, and board members, not-for-profit accounting standards promote transparency, adherence to Generally Accepted Accounting Principles (GAAP), and government compliance. Instead of making a profit, nonprofits funnel as much funding as possible toward their missions to better society and help people in need.

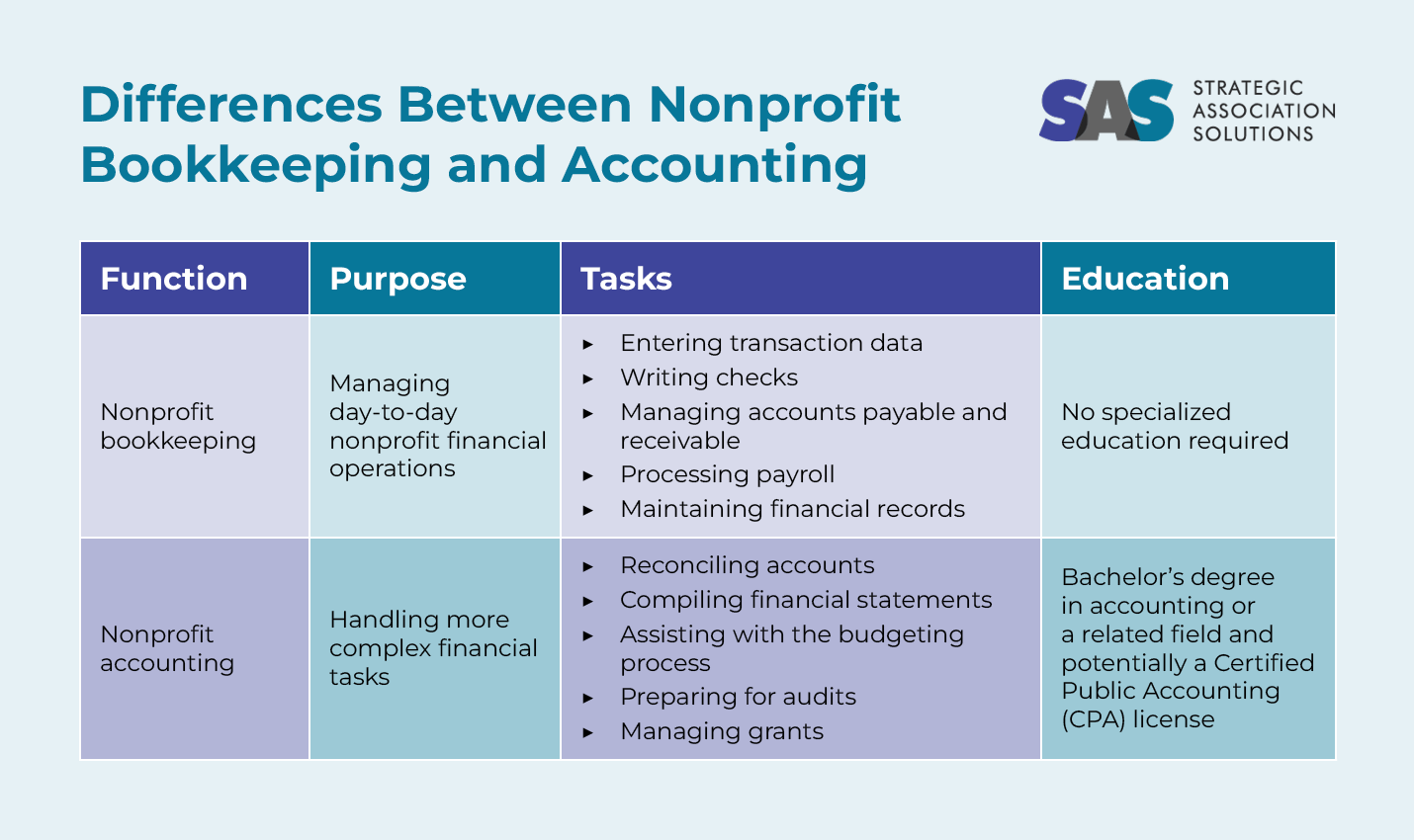

How do accounting and bookkeeping for nonprofits differ?

Accounting and bookkeeping are both elements of financial management, but they have slightly different purposes and functions. Let’s explore the key differences between them:

- Bookkeeping for nonprofits involves managing your nonprofit’s day-to-day financial operations. Your bookkeeper should enter transaction data into your system, write checks, manage accounts payable and receivable, process payroll, and maintain financial records. This role doesn’t typically require specialized education.

- Accounting for nonprofits requires handling more complex financial tasks. Nonprofit accountants reconcile accounts, compile financial statements, assist with the budgeting process, prepare for audits, and manage grants. It’s their job to help your organization maintain GAAP compliance. Accountants usually have at least a Bachelor’s degree in accounting or a related field and may have a Certified Public Accounting (CPA) license.

In addition to a bookkeeper and accountant, you may have a fractional CFO directing your organization’s financial strategy with assistance from your board members, leadership team, and finance committee.

Core Nonprofit Financial Statements, Documents, and Reports

To maintain GAAP compliance and keep your finances organized, your nonprofit must compile several key documents. We’ll review each of these in greater detail.

Chart of Accounts

A chart of accounts lists all the accounts your nonprofit uses to record financial transactions. It serves as the foundation of your accounting system and organizes financial data into different categories for easier reporting and analysis.

The typical categories for a nonprofit chart of accounts include:

- Assets, which are the resources your nonprofit owns, such as cash, accounts receivable, and property.

- Liabilities, which are debts or obligations your nonprofit owes, such as debt, accounts payable, and deferred revenue.

- Net Assets, which are your nonprofit’s available financial resources found by subtracting your liabilities from your assets.

- Revenue, which are funds your nonprofit earns or receives from sources like donations, membership dues, events, grants, and program income.

- Expenses, which are costs your nonprofit incurs, like rent, payroll, and program expenses.

To differentiate accounts and easily navigate your chart, you’ll assign a number to each account. For example, assets may be numbered 1000-1099, and liabilities may be 2000-2099, with subcategories like accounts receivable labeled 1010 and accounts payable 2010.

Nonprofit Financial Statements

Every year, your nonprofit accountant will compile financial statements that summarize your financial performance using different data points and categories. These documents not only allow you to remain compliant with GAAP, but they also organize financial data, making it easier to analyze and report to stakeholders.

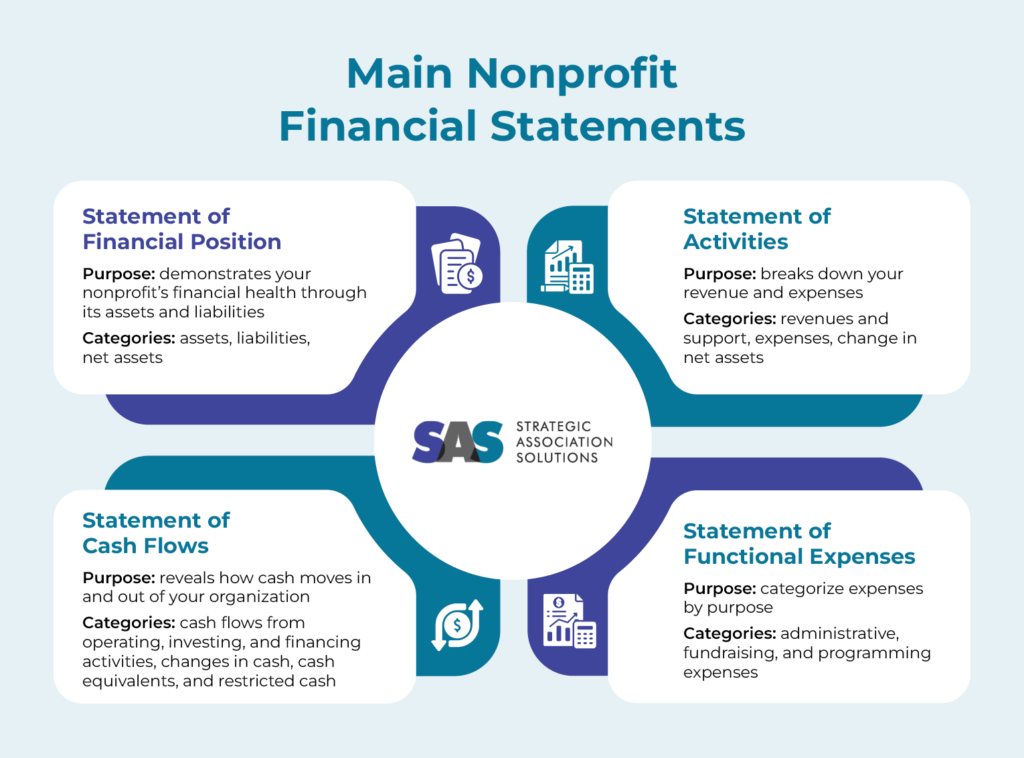

The four main nonprofit financial statements include:

- Statement of Financial Position. Also called a balance sheet, this document demonstrates your nonprofit’s financial health through its assets and liabilities. By subtracting your liabilities from your assets, you’ll calculate your net assets, or available financial resources.

- Statement of Activities. This statement breaks down your revenue and expenses. Known as an income statement in the for-profit world, your statement of activities shows your change in net assets for a certain period, so you can see how your financial resources have changed over time.

- Statement of Cash Flows. This report reveals how cash moves in and out of your organization. It differentiates cash flows from operating, investing, and financing activities, allowing you to understand how much cash you have readily available to pay expenses.

- Statement of Functional Expenses. Nonprofits must provide an expense analysis as part of their annual tax returns. Most organizations choose to do so in a Statement of Functional Expenses that indicates whether expenses are associated with administrative, fundraising, or programming tasks.

In addition to guiding your decision-making and maintaining compliance, these nonprofit financial statements allow you to remain transparent with stakeholders about your finances. By making these documents publicly available, donors, members, and funders can see whether you’ve used their funds appropriately, encouraging them to continue supporting your organization.

Nonprofit Tax Forms

Maintaining tax-exempt status and keeping your nonprofit in good standing requires filling out various tax forms. Each year, your organization will file the following forms:

Form 990

Form 990 is the annual return that tax-exempt organizations must file with the IRS to prove their compliance with their status requirements. On this form, you’ll provide information about your yearly revenue and expenses, board and key staff members, employee compensation, and mission.

Depending on the size of your organization, there are different versions of the form in addition to the standard version, with Form 990-N for small nonprofits, Form 990-EZ for mid-sized organizations, and Form 990-PF for private foundations. Regardless of the form you fill out, you must file it by the 15th day of the fifth month after your fiscal year ends, which is May 15th for most organizations.

State-Specific Tax Forms

Each state has its own tax requirements, which may require your organization to fill out additional forms. These may include:

- State income tax returns to report on unrelated business income (which is any money generated by activities that aren’t central to your nonprofit’s mission)

- State income tax exemption forms to avoid paying income tax

- Sales tax exemption forms to prevent your organization from paying sales tax on purchases made for charitable purposes

- State charitable solicitation registration forms to allow your nonprofit to solicit donations in a certain state

For example, nonprofits in Indiana must file Form NP-20 to apply for sales tax exemption, whereas organizations in Massachusetts only need to send their IRS determination letter and an explanation of their request to the Massachusetts Department of Revenue.

Employer Tax Forms

To provide the necessary information for your nonprofit’s employees to file their tax returns, you must fill out and issue Form W-2 to each employee on your organization’s payroll by January 31st. You’ll also file Form W-3 with the Social Security Administration to summarize all of your W-2s from the year.

If you hire any outside vendors or contractors and pay them more than $600 for their services, you’ll also have to file Form 1099, which reports on the miscellaneous income you pay to these external parties. This form is also due January 31st.

Budget

Your nonprofit’s operating budget guides your financial decisions for the year. It allows you to project revenue and expenses so you can allocate resources accordingly.

Additionally, your organization may compile other secondary budgets, such as:

- Capital budget for long-term projects and investments

- Program budget to organize new program costs

- Event budget to better plan for event expenses

- Grant budget to show how you’ll allocate grant funding

Before creating any kind of budget, it’s best to review past financial data so you can learn from your nonprofit’s previous performance and create a budget that’s both realistic and ambitious. For example, if you earned $20,000 in ticket sales from your last fundraising event, you may project you’ll earn $21,500 this time with a stronger marketing strategy and larger donor base.

7 Nonprofit Accounting Expert Tips

Now that you understand the basics of accounting for nonprofits, consider implementing these best practices into your financial management strategy.

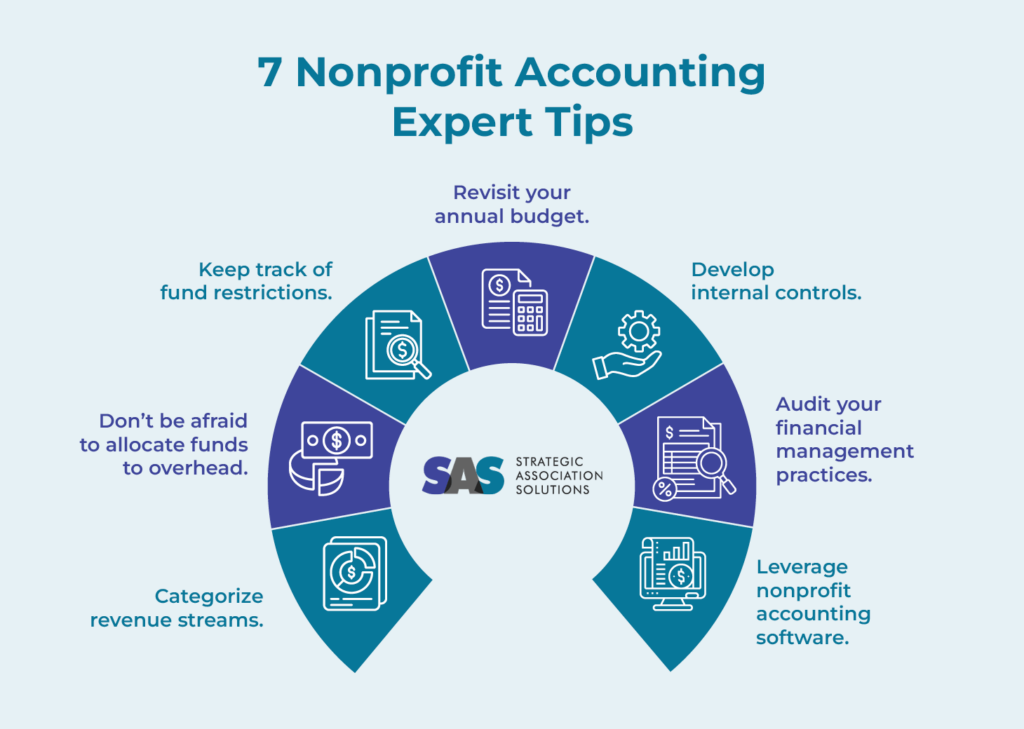

1. Categorize revenue streams.

Diversifying your revenue helps keep your nonprofit financially stable and sustainable. If one revenue stream dries up, you’ll have others to rely on. However, the more revenue sources you have, the more complicated your financial reporting may become.

Categorize related revenue streams to simplify reporting. Keep your financial records consistent by using the following common labels:

- Individual donations, including monetary donations, in-kind gifts, and event revenue

- Corporate philanthropy, including sponsorships, matching gifts, and volunteer grants

- Earned income, including membership dues, merchandise sales, and program fees

- Investments, including endowments, mutual funds, stocks, bonds, and cryptocurrency

- Grants, including those from the government or foundations

Dividing revenue in this way also streamlines financial analysis. By grouping like revenue sources, you can easily compare their performance and determine where to direct your attention.

2. Don’t be afraid to allocate funds to overhead.

In the past, many organizations have tried to limit overhead funding as much as possible, seeing it as money that could be better allocated to their missions. While you should try to maximize the funds that go toward your cause, you can’t properly pursue your mission without putting enough funding toward the behind-the-scenes processes that keep your organization running smoothly.

Think of it this way: how would your nonprofit run without the right people, space, and tools to execute your mission? Short answer: it wouldn’t.

Overhead funding includes administrative and fundraising costs—essentially everything besides programmatic expenses. Items that fall under this category include employee compensation, office rental, and fundraising software costs.

While experts once estimated that nonprofits should limit overhead expenses to under 35% of funding, increasingly more organizations recognize that an ideal overhead cost breakdown doesn’t exist. Every nonprofit should determine how much it can realistically allocate to overhead while still prioritizing programmatic expenses.

3. Keep track of fund restrictions.

Some donors may want you to use their funds for a specific purpose or time period. These stipulations are known as donor restrictions, and following them allows you to maintain trust with stakeholders and build strong relationships.

Ensure you adhere to donor-imposed restrictions by using the following categories within your accounting system:

- Unrestricted funds. These funds have no limitations, so you can use them however you’d like. Most small and mid-level individual donations fall under this category, as these supporters typically contribute directly through your donation page.

- Permanently restricted funds. These funds have limitations that your nonprofit must follow indefinitely. For example, you may set up an endowment fund to support your nonprofit’s scholarship program. All donations made to your endowment fund will go to providing scholarships to students in need.

- Temporarily restricted funds. These funds have limitations, but after the project they’re meant for is finished or a certain time period passes, the leftover funds become unrestricted. For instance, if a company sponsors your association’s conference and you have unspent funds afterward, you can use these contributions to support overhead or other programmatic expenses.

Your chart of accounts should have separate account categories for restricted and unrestricted funds, with subcategories for permanently and temporarily restricted funds. You should also keep detailed transaction records to ensure you use funds according to donors’ intentions.

4. Revisit your annual budget.

While you’ll go through the budgeting process annually, that doesn’t mean you can only change your budget once a year. Each month, revisit your budget with your team to compare your budgeted revenue and expenses to your actual revenue and expenses.

By building budget analysis into your regular schedule, you can pinpoint any deviations from your expectations and adjust your resource allocation accordingly. If you have any unexpected revenue or expenses, you can also add those at this time.

5. Develop internal controls.

Internal controls are practices that help you prevent theft, detect fraud, and identify any errors. Instill proper checks and balances within your financial management strategy by:

- Creating financial policies. Align your team with standards for handling different financial management situations. Your policies and procedures should cover areas like expense approval, cash handling, payroll processing, budget management, and financial reporting to standardize these operations.

- Separating financial duties. No one individual should have complete control over your organization’s finances. Separate tasks involved in different financial processes to prevent mismanagement. For instance, the same team member who manages cash receipts should not also reconcile accounts.

- Protecting physical assets. In addition to your financial records, you’ll also have to protect physical assets. Use safes or locked cash boxes to store cash and checks securely. Additionally, track inventory of valuable office equipment like computers and cell phones.

With proper internal controls, you can rest assured that your financial records are accurate and that team members are accountable for their responsibilities within the financial management process.

6. Audit your financial management practices.

While the tips in this guide will help you tighten up your accounting and financial management strategy, an external audit verifies that your nonprofit follows best practices, has accurate financial statements, and remains financially sound.

There may be situations where you’re required to conduct a financial audit, such as receiving a significant amount of federal funding, taking out a loan, or applying for a grant. Even if not required, financial audits allow you to identify risks, improve your strategy, and maintain transparency with stakeholders.

7. Leverage nonprofit accounting software.

The right tools will help you track all financials so nothing falls through the cracks. Leverage a nonprofit-specific accounting solution (like Aplos) or accounting software with nonprofit features (like QuickBooks or NetSuite) to manage revenue and expenses effectively.

For instance, instead of manually tracking restricted funds, accounting software can automate this process by automatically categorizing and allocating restricted funds. Investigate different options, and ensure the solution you choose integrates with your constituent relationship management platform (CRM) for easy data transfers.

Specific Accounting Considerations for Associations

Due to their structure and activities as membership-based organizations, associations and professional societies have their own unique accounting considerations. If you run a membership-based nonprofit, you’ll need to take care to address these areas:

- Recognizing revenue from multiple sources. Associations especially have many revenue streams, from membership dues to sponsorships to events. Establishing when and how to recognize each revenue source can be difficult for organizations with little to no accounting experience.

- Accounting for membership dues. Members pay dues on a recurring basis. That means membership-based organizations need to understand how to manage recurring payments, recognize deferred revenue, and keep track of lapsed memberships and unpaid dues.

- Navigating compliance with tax laws. While all nonprofits are subject to various tax laws, adhering to these regulations can be more complex for associations. For example, associations may be more likely to pay unrelated business income tax (UBIT) if they sell advertising space in their membership materials or on their websites. Additionally, relevant tax legislation is currently in flux, and some have proposed taxing all non-donation revenue streams, including membership dues, sponsorships, and educational program revenue.

- Managing the financial implications of association mergers and acquisitions. Sometimes, associations with similar missions combine to do more for their communities. These business decisions complicate financial management, necessitating asset allocation, fund consolidation, and alignment of both organizations’ financial goals and accounting methods.

- Handling large event financial management. Many associations hold conferences and other major events. While these events generate significant revenue, they also make financial management more difficult by having to account for multiple revenue streams and develop a successful budget.

- Reporting for multi-department associations. Large associations typically have different departments for different functions, like membership, events, advocacy, and education. If each department has its own budget and financial needs, it can be difficult to streamline reporting.

While you may be able to handle these challenges on your own, your best bet is to work with association accounting experts. Let’s explore your options for doing so.

Working with an Association Accounting Expert

When hiring accounting staff, you have several options for sourcing new team members:

- Hiring a full-time accountant. Adding a full-time in-house accountant to your team allows large nonprofits to gain access to professional expertise. However, hiring a new employee can be expensive and time-consuming, taking funds and time away from your mission.

- Securing an in-kind donation of accounting services. You may be able to find a volunteer who’s willing to lend their expertise to your organization for free. This option may work well for newer organizations or one-time projects, but it’s often unsustainable, as the professional will likely want to be compensated for their time eventually.

- Outsourcing the work to a membership-based nonprofit accounting firm. The best option is to outsource your accounting function to a dedicated firm. That way, you’ll unlock expertise at a lower cost and be able to adapt the services you need as your organization grows.

We strongly recommend working with a dedicated nonprofit accounting firm, and look no further than the experts at Strategic Association Solutions (SAS). Our team is focused on providing high-quality nonprofit accounting services and back-office solutions for membership-based organizations.

We understand the unique challenges membership organizations face and can customize our services to your nonprofit’s needs. Plus, we provide a variety of additional services, including strategic consulting, technology support and systems implementation, payroll and human resources support, and design services, to round out your overall association strategy.

Partner with the Accounting Experts at SAS

Nonprofit accounting is complicated and even more so when you run a professional society or trade association. Between budgeting, reporting, compliance, and more, there are so many nuances and tasks required for proper association financial management.

If you need help organizing your association’s finances, our team is ready to assist! Fill out our contact form so we can discuss our membership-based nonprofit accounting services and back-office solutions and customize them to your needs.

To learn more about SAS before moving forward, check out these additional resources:

- Nonprofit Accounting Services & Back-Office Solutions. Dive deeper into SAS’s full array of nonprofit accounting services and back-office solutions to see how we can help your membership-based organization.

- About Us. Learn more about our approach and team.

- Who We Serve. Discover the types of organizations we serve and how we have helped nonprofits in the past.

Effie Panos

Principal

As a self-starter and team player, Effie brings a blend of management and extensive accounting experience, with expertise in financial management, Generally Accepted Accounting Principles (GAAP), operations, change management, budgeting, forecasting, and revenue optimization to clients.

Effie holds a Bachelor of Science in Accounting from the University of Illinois. She has held many previous roles in nonprofit accounting and operations, most recently as a Controller for A Safe Haven Foundation and Vice President of the Not-for-Profit Division at Quattro Business Support Services.